The stay’s scope is broad: it enjoins unsecured creditors from judgments and collection suits, halts secured creditors’ repossession and foreclosure proceedings, and pauses IRS tax levies and liens—with narrow exceptions for support obligations and certain tax assessments. The stay does not eliminate debt; it suspends collection enforcement, giving bankruptcy priority over individual creditor recovery. Violations expose creditors to sanctions and damages.

The stay does not enjoin all creditor actions. Criminal prosecutions proceed unimpeded. Support obligations—child support and alimony—remain enforceable because federal law prioritizes family support. Tax authorities may continue certain administrative proceedings and audits, though collection is paused. Landlords holding final judgments for possession may continue eviction. In cases of repeat filings within one year, the stay’s duration is substantially curtailed unless the debtor demonstrates extraordinary circumstances justifying extension.

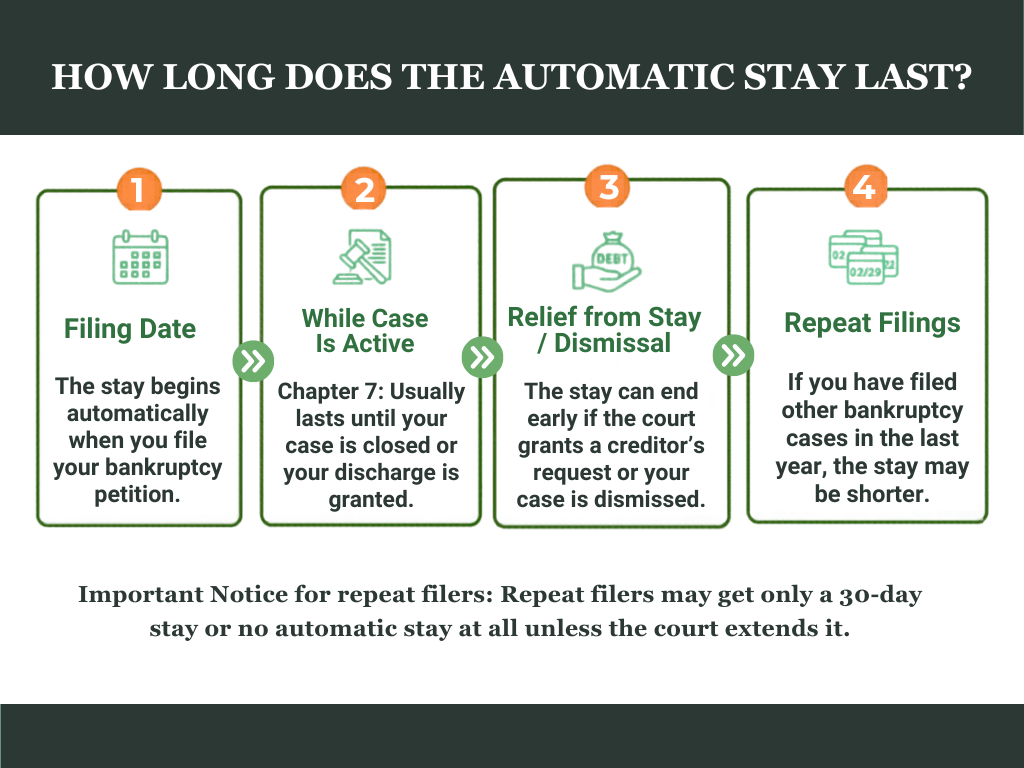

In Chapter 7, the stay remains in effect until case closure and discharge. In Chapter 13, the stay continues throughout the repayment plan unless a creditor petitions for relief based on changed circumstances. Upon dismissal, the stay terminates immediately. Repeat filers face abbreviated stay periods under 11 U.S.C. § 362(c)(3) and (4), requiring statutory findings to extend protection.